Traveling to China is an incredible experience, but like any international trip, unexpected events can disrupt your plans. From sudden illnesses to flight cancellations or lost luggage, having the right China travel insurance is not just a smart backup—it’s a necessity for peace of mind. Many first-time visitors underestimate the complexity of China’s healthcare system for foreigners, where upfront payment is often required at international hospitals. In this guide, I’ll walk you through the key aspects of China travel insurance, including mandatory requirements, medical coverage, how to choose a policy, and common exclusions. By the end, you’ll know exactly what to look for before booking your flight.

Is China travel insurance mandatory for foreigners

For most tourist and business visa holders, China does not legally require travel insurance at immigration. However, certain visa types—such as the 144-hour transit visa or long-term residence permits—may ask for proof of health coverage. More importantly, while not mandatory, hospitals in China almost always demand upfront payment from foreign patients. Without insurance, a simple emergency room visit can cost hundreds of dollars, and a serious hospitalization might run into tens of thousands. Additionally, if you plan to visit remote areas like Tibet or Xinjiang, local authorities sometimes request proof of insurance for rescue services. So even though it’s not a legal must,skipping China travel insurance is a financial risk no smart traveler should take.

What medical expenses China travel insurance covers

A good China travel insurance policy typically covers emergency medical treatment, hospital stays, ambulance fees, and prescription drugs. Many plans also include evacuation to your home country or to a better-equipped facility if local care is insufficient. For example, if you break a leg while hiking the Great Wall, your insurance can arrange airlift to a top-tier hospital in Beijing and cover the bills. Dental emergencies from accidents, like a knocked-out tooth, are often included as well. However, routine check-ups or elective procedures are usually excluded. Always check the policy’s maximum limit—aim for at least $100,000 in medical coverage because China’s top international hospitals (like United Family) charge Western-level prices. Some plans also offer 24/7 multilingual hotlines to help you find English-speaking doctors, which is a lifesaver in a crisis.

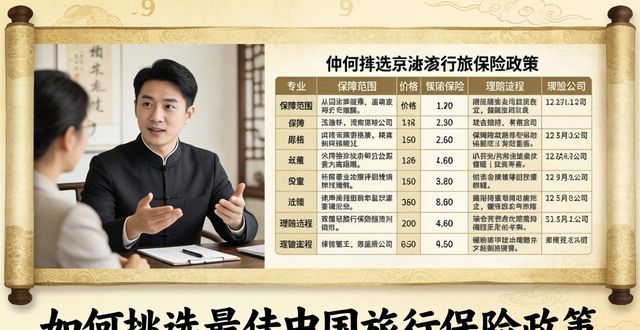

How to pick the best China travel insurance policy

Start by comparing three core features: medical coverage limit, deductible amount, and emergency evacuation benefit. For China, look for a policy that explicitly covers “pre-existing conditions” if you have any, as many standard plans exclude them. Next, check whether the insurer has direct billing agreements with hospitals in major Chinese cities like Shanghai, Beijing, and Guangzhou—this saves you from paying upfront and filing claims later. Also, pay attention to adventure sports coverage: if you plan to ski in Zhangjiakou or scuba dive in Hainan, make sure those activities are not excluded. Read online reviews from other travelers, but be wary of fake testimonials. Reputable providers for China include World Nomads, Allianz, and Ping An’s international plans. Finally, verify that the policy covers trip interruptions caused by China’s unique weather issues, such as typhoon cancellations or smog-related flight delays.

Common exclusions in China travel insurance policies

Even the best China travel insurance has limits. Almost no policy covers injuries from extreme sports like bungee jumping or rock climbing unless you buy a separate “hazardous activities” rider. Pre-existing chronic conditions (diabetes, asthma, heart disease) are routinely excluded, though some insurers offer a waiver if you pay extra. Alcohol or drug-related incidents are never covered—so don’t expect reimbursement if you get into a bar fight or fall off a motorbike while drunk. Also, many plans exclude epidemics or pandemics; check the fine print for any mention of “public health emergencies.” Theft of unattended baggage is often capped at a low amount, and expensive items like laptops or cameras may require a separate rider. Finally, treatments from local Chinese medicine clinics or unlicensed practitioners are generally not reimbursed. Understanding these exclusions helps you avoid nasty surprises when filing a claim.

Have you ever had a medical emergency or travel mishap in a foreign country? Share your experience in the comments below—your story could help fellow travelers prepare better. And if you found this guide useful, please like and share it with anyone planning a trip to China. Safe travels